Deep Dive: Heartland Express (NASDAQ: HTLD)

Deep Dive #2: Heartland of a heartless subsector (for-hire truckload)

Heartland (“$HTLD”) is a good operator in one of the toughest subsectors of the transportation industry: for hire truckload. If you’re a long-term, buy-and-hold generalist investor, it may make sense to skip over companies in this sector altogether as severe fragmentation combined with asset-intensity makes it difficult for any company build out a sustainable, competitive advantage.

In spite of inhospitable conditions, Heartland has managed to carve out a decent niche. It’s conservatively financed, family owned, and has an intense focus that differentiates it vs. many of its peers.

I’m going to spend more time on the industry here than with Old Dominion, as differentiation between companies in for-hire truckload (“truckload” or “TL”) is less pronounced than in less-than-truckload (“LTL”).

Truckload is the largest investable subsector on a revenue basis within trucking (“Private” consists of fleets owned by companies like Wal-Mart and so are not directly investable). Truckload carriers (“carriers”) move a single shipment for a single customer (“shipper”) from point A to point B.

The challenge for most truckload carriers is utilization, specifically handling what’s called the backhaul. In the diagram below, point A is typically a “headhaul” market where there is more freight headed outbound than inbound. A prime example is Los Angeles, where Asian imports outweigh U.S. exports. Thus it isn’t terribly difficult to find customers wanting to book your “headhaul” as there’s more shippers looking to ship goods than carriers offering trucks to move them. However once your truck and your driver are at point B (e.g.: Las Vegas), the backhaul is complicated because:

You’ve got a driver on board that has to return home to his/her family, eventually.

There’s typically less freight to take you back.

Ideally, as a trucker you’d book freight at a lower rate in the “backhaul” lane. However, there will be times when the truck has to run empty the entire way back, the industry term for this is “deadhead”. This isn’t to say this is a complete loss to trucking companies: the industry is often well aware of the limited opportunities to get back so trucking companies try to charge a premium for headhauls to destinations where booking return freight is difficult.

The above assessments is made all the more complicated due to the fragmented customer (shipper) and supplier (carrier) bases. The largest truckload carrier, $KNX, accounts for just over 1% of industry revenues. So it’s very hard for shippers and carriers to find each other. If you’re thinking that there should be a technology solution to this, you’d be right: there are “traditional” truck brokers, low-service internet “load boards”, and a ton of tech startups who specialize in making these connections. We’ll cover a broker in our next deep dive.

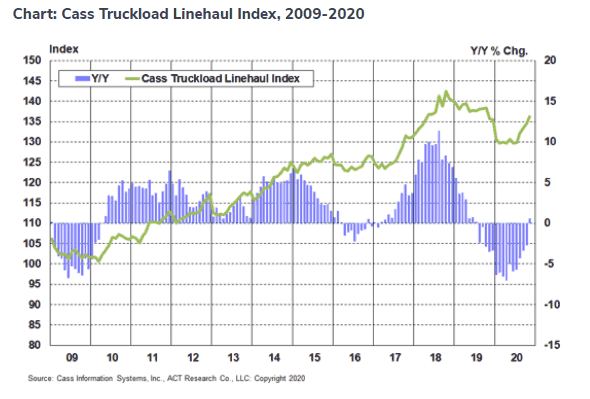

Truckload is a tough business, because while there are some benefits to scale, from an operational perspective the largest truckload carriers don’t differ all that materially compared to a single truck driver owner operator running his/her own truck: no matter what you’ve got to drive a truck from point A to point B and make it back to point A. This limited scale benefits is why the fragmentation is pretty astounding: 90% of industry capacity in trucking companies which operate 6 or fewer trucks. If you look at long-term industry pricing, it’s almost a textbook case of perfect competition: the industry generally feasts when the economy is accelerating and starves when the economy slows. Pricing regularly oscillates from +5% to -5%, and sometimes more, and on a 10-year CAGR is about 2.8% between the beginning of 2010 and end of 2019.

But even so, there’s always hope that there exist individual truckload companies, running very unique strategies, could potentially buck the trend because up to now we’ve been discussing “averages.” As we shall soon see, Heartland does make a conscious effort to differentiate themselves. However, I think the evidence on the balance is that any advantages that may exist are not significant.

Ok, time to get to the heart of today’s article, a deep dive on Heartland Express. $HTLD’s strategy, summarized:

Focus: Rigorously focuses on less than 500 mile lanes with non-perishable goods that require high service levels, including “just-in-time” deliveries. This should result in a business that has better pricing.

Profitability: Long-term adjusted operating margin target of 15%+.

Conservative financing: No net debt. Ever.

Significant “Growth”: I’m…perplexed? Personally not seeing the growth in the numbers…

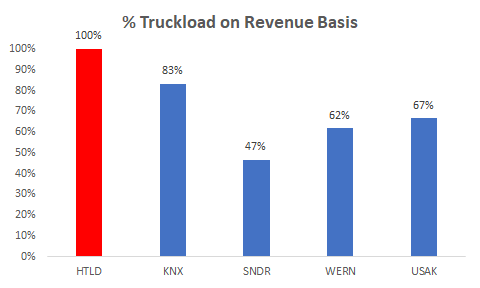

I want to emphasize that it’s rare to see a truckload carrier this focused: $HTLD almost exclusively focuses on dry van truckload (the familiar trucks you see similar to the one in the picture above), with a very small temperature-controlled segment which was reduced to serving select customers in 2019. In fact, they exited their non-asset based services segments in 2017 (twice in fact due to an acquisition!). This contrasts with most of the other large public carriers who often are involved in quite a few lines of businesses of which truckload is merely the largest:

$HTLD also specifically focuses on the less than 500 mile high service regional lanes. The shorter hauls should help with driver retention, as most drivers prefer to go home when they can, especially for drivers with families. Realistically, a company driver at the higher end of the 500 mile range can expect to be home every other night at a minimum, as driving nonstop for 14 hours, the max allowable by law, at 70 miles per hour covers 980 miles. This isn’t realistic in reality because it’ll also take time to load and unload the truck as well as bathroom breaks, etc.

The profitability target is interesting, especially since it’s a lot better than most of their competitors. Despite having the highest margins, returns on capital and returns on equity are only middling. Part of this I believe is that most of the other trucking companies have less asset intensive businesses such as truck brokerage.

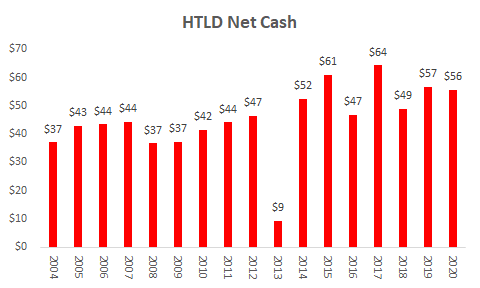

$HTLD has held a net cash position for 16+ years. The rare blip you see in 2013 was when they made their largest acquisiton of Gordon Trucking for $300M in November 2013.

Finally, it’s a bit surprising to see “significant growth” cited as a long-term strategy by $HTLD in their 10-K, as over the last 16 years they’ve grown revenues at a rather pedestrian 2.2% CAGR. Diluted EPS growth is also around 2% CAGR. While they are definitely growing, but I wouldn’t consider the growth to be significant.

While we can quibble over the stated significant long-term growth goal, management incentives are quite clear. Management and directors own 39% of the company in aggregate, or over $600 million worth, almost all of which is held by the CEO and family members who together founded the company. This makes it easier to believe their claim:

“We manage our business primarily based on long-term cash flow generation prospects and return on equity, and we place less emphasison quarterly earnings per share.” -2020 $HTLD 10-K

Let’s revist the key question: does Heartland have a sustainable competitive advantage? The answer is…maybe. But even if it exists it is not strong. Here’s the evidence:

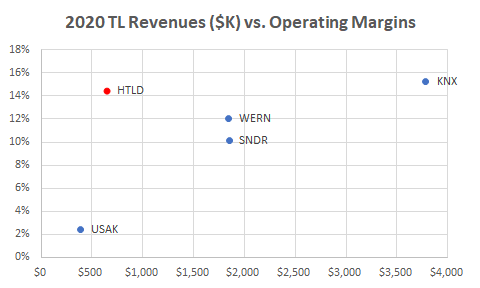

Drawing truckload revenues and operating margins for the public carriers on a scatterplot excluding $HTLD, there appears to exist a positive correlation between revenues and operating margins overall which suggests there may be some scale advantages for truckload operations. However, $HTLD really messes this up as an outlier, and based on my recollections $USAK hasn’t been the best run historically.

Source: Company Filings $HTLD made a major acquisition of Gordon Trucking, which expanded their presence to California in 2013 (previously business was primarily east of the Rocky Mountains). The acquisition was for $300M, relative to an EV of about $1B as of 9/30/13, so it expanded the company by about 30% (the market rewarded the acquisition with a 50% bump). However, even years after, we’re not seeing any sort of difference in the operating margins. If anything it looks like operating margins have deteriorated:

Source: TIKR.com, HTLD press releases $HTLD engages in pro-cyclical behavior as well, characteristic of a relatively commoditized business. They state in their K that:

“When we are experiencing or expect favorable freight markets, we invest in fleet expansion internally, dependent on our ability to hire drivers that meet our qualifications, and through acquisitions. When freight markets are less favorable, we concentrate our assets on customers offering the most acceptable returns and are willing to shrink our fleet to maintain margins and limit net capital expenditures.” -$HTLD 2020 10-K

So let’s summarize.

The good news:

$HTLD continues to execute a disciplined strategy fairly well.

There’s a clearly articulated desire to manage for long term cash flows.

High insider ownership aligns incentives between minority shareholders and management.

High operating margins compared to competitors.

The bad news:

It’s a tough subsector to operate in, and operating margins and ROEs across the industry reflect this.

Even $HTLD admits to partaking in pro-cyclical behavior, expanding when conditions are good and shrinking when conditions are bad.

Thus overall it’s tough to view $HTLD, and more generally companies in the for-hire truckload sector, as investments rather than trades.

Not investment advice. I’ve actually never owned a truckload company in my life…Family members continue to own shares in $ODFL.

Appendix:

One way to demonstrate that truckload is less differentiated than less-than-truckload is to observe stock returns of companies within each sector. There is a much narrower dispersion in 10-year stock returns for companies within the truckload subsector vs returns for companies within the less-than-truckload subsector:

Here’s the stock performance of the truckload sector over 10 years (March 2011-March 2021):

And here’s the less-than-truckload sector (March 2011-March 2021):

If you invested $100 at the beginning of the 10 year period, the difference in truckload between the best performing and the worst performing stocks is about 2.4x ($278 vs. $114), while the same comparison in less-than-truckload is an incredible 1,600x ($1,920 vs $1.14). Even if you ignore the underperformer in less-than-truckload, $YELL, it’s insane that the best-in-class operater in LTL saw 1,821% cumulative 10-year returns, or 34% CAGR, while the best performer in truckload had a more normal 11% CAGR.

Good analysis of industry dynamics