Reaction: Impact of Containership Stuck in the Suez Canal

New series with takes on big transport events. Starting with the trouble in the Suez (h/t Billy Joel).

If you haven’t heard, a ginormous 20K TEU Suez-Max container ship has gotten stuck in the Suez Canal. It’s been quite the muse for memes. I’m going to try to give you the investor/operator-oriented perspective, starting with some quick hits, continuing with discussing the implications, and wrapping with some winners and losers.

Quick Hits:

“Ever Given” (the name of the stuck ship) is tied for the 66th largest completed containership in the world. It has 20,124 TEU in capacity. “TEUs” are an industry term meaning “Twenty-foot equivalent units,” reflecting the length of a common type of shipping container.

It typically takes 25-30 days to move freight from Shanghai to Rotterdam. It takes an additional 13 days to go around the southern tip of Africa.

A commonly cited statistic estimates that 80-90% of world trade touches a ship, and 10-12% of total global trade goes through the Suez which is a crucial artery for moving goods between Asia, Europe, and the east coast of North America.

$6-$10B of “lost trade” a week according to Allianz

$10B of goods held up per day. My math suggests this is actually low looking only at the containership piece (not considering commodity products transported via bulk carriers):

Now that we’ve got the quick stats out of the way, as a shipper what can you do about it?

Shipper Alternative Choice 1 (of 2): Airfreight

Aside from the decision to wait or go around the southern tip of Africa, if you really need the goods in a hurry you’re going to have to take to the air, as Peloton has already done due to ongoing supply chain issues and Caterpillar is reportedly considering doing to avoid factory production shut-downs.

The two issues with shifting to airfreight are:

It’s really expensive. The heuristic is that airfreight is about 8-14 times more expensive than ocean freight. Indeed, Peloton stated that their transportation costs would be 10x higher, but I believe that’s a total figure includes last mile delivery and also includes some shipments being shifted to expedited ocean which is expensive but not as expensive as airfreight. Thus the true dollar increase from shifting the ocean component of the move to airfreight freight will be higher yet.

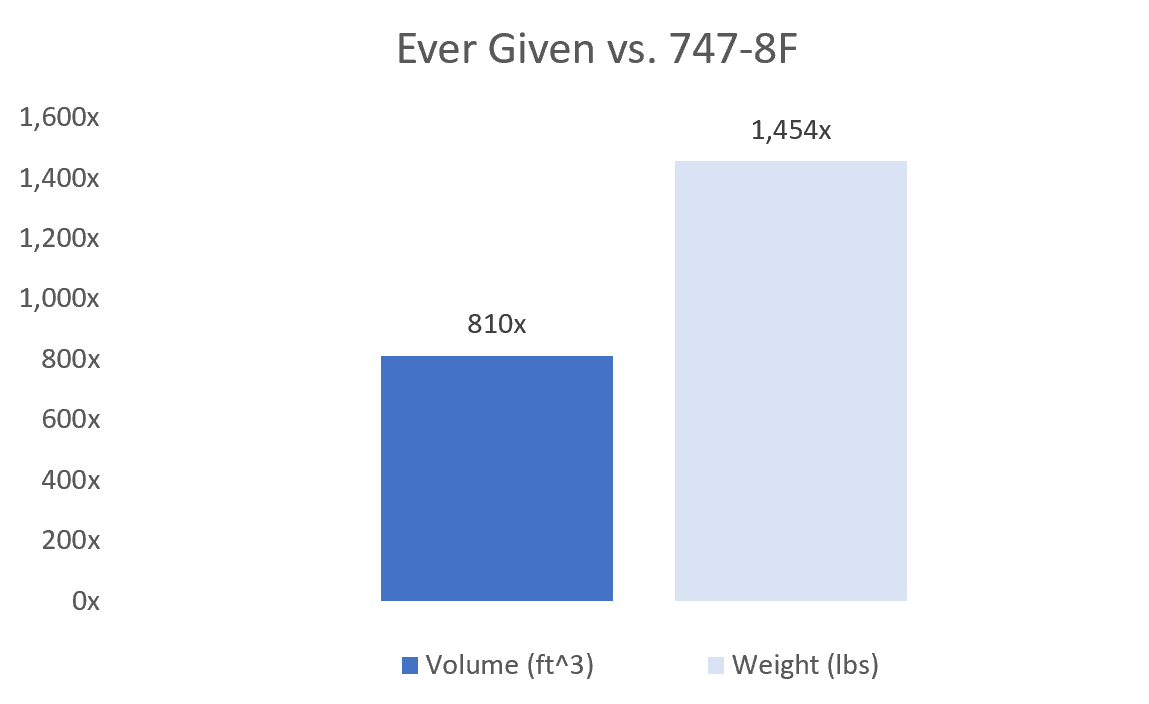

A ship is waaaay bigger than a plane. It would take over 800 747-8Fs (which is the biggest commercial cargo plane that’s widely used) to carry the same volume of freight as a ship as large as Ever Given, not to mention weight differences. There are only 141 747-8Fs in the world and an additional 170 of the smaller 777Fs and 126 even smaller 747-400Fs. So all the world’s long-haul freighters combined likely wouldn’t be enough to replace the Ever Given. And this is only one container ship, globally there are 77 total container ships with over 20K TEUs in capacity, each and ~36 times the capacity of Ever Given stuck outside the Suez in aggregate currently.

I suspect by this point most shippers and astute fast money hedge funds have figured out that 1) some shippers will have to go to the air, and 2) spot airfreight rates will likely rise further due to the supply demand imbalance.

Shipper Alternative Choice 2 (of 2): Rails

Railroads are being cited as another alternative for shippers. While this is more plausible, it has it’s own hurdles.

As background, a railroad intermodal container is a 53 foot container, so typically you can fit roughly 3 40 foot oceanfreight container items into a 2 53 foot railroad intermodal containers, roughly. Railcars typically average 70 cars (but can certainly be longer), which works out to roughly 100 40 foot containers. Given that Ever Given’s capacity is about 10K 40 foot containers, you’d need 100 trains of 70 rail cars each to replace one Ever Given. That’s quite a bit, but not as insane as airfreight.

The issues with rail:

Time for freight already en route. While airfreight can get virtually anywhere in a day or so, shipping by rail takes 15-18 days to get from China to Europe. But for some shippers this is after you’ve already waited around 20-25 days as your shipment via ocean freight has chugged its way from China to the entry to the Suez Canal. So, even if you could immediately put stuff on the rail, you’d still be a week or two late. Not to mention you’re likely fighting for capacity and equipment with countless other shippers attempting similar strategies.

You may not even have the goods ready to ship. Your just-in-time manufacturing process may have been planned to get the exact amount of goods ready to ship by ocean freight for this month. And now that entire shipment is hanging out amongst thousands of other boxes on Ever Given or another containership, so if you want to replace it via a rail shipment you’ll have to manufacture everything again.

While I’m sure some shippers will use rails for shipments they were planning on sending out soon, making up for freight already on the way seems difficult.

Intermediate Term Ripple Effects Expected

A good way to analogize the situation is to consider what happens after a big event such as a sports event, conference, or music festival. Because everyone leaves immediately after, you get this massive pile up that looks something like this:

With these types of events, you’ll likely also see ripple effects at downstream highways, airports, etc. as the surge emanates outwards. This causes congestion and “surge” pricing which progressively dampens as you get further and further away from the root cause. We should see similar ripples with the Suez issue. Once the ship is moved, the freight should impact in progressively lessening degrees:

Ports

Drayage providers (moves freight from ports to local warehouses)

Warehouses close to ports

Trucking/Domestic air carriers/Rails

Warehouses close to end customers

Last mile delivery providers

Consumers like you!

Freight also generally requires equipment to help move (containers, trucks, trailers, boats, etc.), which poses additional complications:

They generally require equipment to help move (containers, trucks, boats, etc.). These equipment can get “stuck” somewhere and become unavailabel, such as on a boat waiting for the Suez to re-open or going the long way around Africa.

Physical goods often have persistent flows in a single direction (out of Asia, to Europe or North America). Thus equipment must be repositioned consistently as they tend to pile up in certain areas with more inbound freight vs. outbound freight.

Both of these will prove to be a challenge even if the Suez Canal blockage is solved today, and will worsen the longer this persists. So this will likely impact ocean freight pricing in the near term as well until equipment imbalances moderate. It’s interesting to note that a similar effect can be observed with NYC’s bike share program, as people generally prefer to ride bikes downhill vs. uphill.

Point of Comparison: West Coast Port Strikes

One historical comparison is the 2014-2015 International Longshoremen’s and Warehousemen’s Union’s labor dispute. The labor union’s contract with the ports expired June 30, 2014, and port productivity worsened until a contract was agreed to February 20, 2015. Note that this was an extended slow down that some foresaw, which is slightly different from the Suez issue where freight movement has all but stopped with little warning.

Looking at loaded import ocean freight TEU data, volumes at the Port of Los Angeles decrease markedly in January and February of 2015 when the situation got really acrimonious, and volumes improve dramatically in March 2015 (up 32% y/y) after a tentative agreement was reached February 20, 2015:

Winners (if you’re confused on what the heck a “freight forwarder” or a “truck broker” is, check out my reference post!)

Airfreight, in particular charterers and other emergency-type cargo carriers will benefit in the near term ($AAWW, Asian cargo carriers).

Air and ocean freight forwarders who have high service quality, such as $EXPD and $KNIN. These specialize in handling difficult situations for customers, and thus take temporary market share in times of stress as lower service quality forwarders and the carriers may underwhelm. I also suspect that high service forwarders use stress situations as a opportunity to show their value and take share from competitors. If you look at the chart below, you can see a few quarters of extemely strong performance from $EXPD post West Coast Port contract issues (weakness in 2016 was due to tough comps combined with a “freight recession”).

Other Third Parties. The general rule of thumb is that brokers and third party providers generally tend to benefit to varying degrees when things are disrupted. For example, perhaps your emergency shipment you had $EXPD set up ends up at an unfamiliar airport so you need a truck broker like $CHRW or $LSTR to help secure some one-off capacity. Other parties that could benefit include shipbrokers and data providers like $BMS.L and $CKN.L.

Losers

Retailers, especially those already short on inventory relative to demand.

Shippers with perishable freight, livestock, or other time-sensitive freight (the last one is not likely given that if something is time sensitive it rarely would go on a boat to begin with).

Manufacturers (including automakers) with components necessary to keep factories running.

Undecided

Ocean carriers is one I struggled with. At first I was pretty sure they’d be a net beneficiary, as they should benefit from better rates. However, they may also incur costs for the cargo stuck in transit. From my reading ocean freight carriers can either declare force majeure if it’s a short term issue or ask cargo owners to help out financially if it takes longer, which should limit the losses. I still think it’s probably a net benefit for ocean freight.

Well That’s A Wrap!

It’ll be interesting to see when we finally manage to unstuck the boat, and the subsequent consequences. Freight is a dynamic system, so there’ll be things that I get right and things that I’ll get wrong I’m sure.

With regards to this series specifically, my goal will be to put together some thoughts for (very) material events in a post similar to this one. I prefer to think over react and thus will be focusing on putting together deep dives ($HTLD is upcoming in a week or two), so please don’t expect frequent posts like this one.

Thanks for reading!

I’m long a starter position in $CKN.L. I’m short a very small amount of Peloton ($PTON) on a lark which has been entertaining but marginally unprofitable. I’m considering $EXPD as a long-term investment but have no position yet.

Bonus Interesting Concept #1: “You’re gonna need a bigger boat”

Ocean containerships have been getting bigger over time (see chart below), driven by intense competition across ocean freight companies to lower the unit cost of shipping a container. The thining goes: “Well prices are drifting lower, but if we build a bigger boat we can lower our cost per container shipped and thus (finally) turn profitable at current prices!” So boats got bigger and bigger over time:

While in theory this should work, the issue is that this is a fragmented industry and everyone undertook similar analysis and drew similar conclusions. So eventually what happens is that everyone ends up with bigger boats in addition to their legacy fleet (less some scrapping). And overall you can see that prices generally drifted downwards since 2006, up until the most recent spike due to stimulus-driven supply chain issues.

Bonus Interesting Concept #2: But maaaybe bigger isn’t always better

In containerships there are also diseconomies of scale. Namely, the more containers you can carry, the more complex it is to handle at the ports. Think about it this way: if a boat carries 3 containers stacked on top of each other and stops at 3 destinations, ideally you’d only need to make one move per destination. Even if you mess something up and/or plans change (say the owner of the last container decides they actually want to have the cargo dropped off at the first port), it’s not a complicated procedure.

However if you go up to 10, 100, 1,000, 10,000, etc., it gets exponentially more complicated. 3! is 6 but if you type in 10,000 factorial (number of possible arrangements for 10,000 containers), most calculators (including Excel) explode. In practice of course, it’s not as complicated, generally you put the containers that will be taken off at the last port towards the bottom.

There are equivalent issues on the port side: the more containers coming off of one ship, the more variability in the number of containers to maneuver on land.